There are billions of pounds, currently, sat in bank and building society accounts earning nothing or very little and this has been the case for a number of years. Although these will not fall in value they can very much be eaten away by inflation.

Although emergency cash is very important to cover any unforeseen costs or a period of unemployment the amount that is available to deal with these situations is, for the most part, much more than is needed.

Once we discuss this area with a client and ascertain the amount of emergency funds they actually need and are happy and comfortable with this we then have to decide on where these extra funds can be invested.

There are many areas that we as financial advisers have to take into account including the client’s attitude to risk; capacity for loss; objectives and goals and what they want to achieve with the investment and how long before it is likely to be used.

Once the right investment vehicle has been recommended then the next step is to make sure that it is reviewed at least once a year to check whether circumstances are still the same as before and that all the areas mentioned, above, have not changed.

Patience is very important when invested and ignoring, as much as possible, the ‘noise’ surrounding the journey an investment will have over the years. By noise, we mean the headline news that we are bombarded with on a daily basis which may affect investor sentiment and, therefore, investments. These events could be reports showing major potential conflicts happening around the world, such as the Russian forces build up on the Ukrainian border, or interest rates going up and inflation spiralling out of control and of course, nearly two years ago, the pandemic and the subsequent lock downs which triggered a very swift fall in worldwide stock markets.

This is where ongoing investment advice is so important making sure that clients do not panic and drastically de-risk their investment or indeed cash it in to avoid, what they believe, could be further losses. If they had managed to do this, without advice, during the market lows of March/April 2020 then they would have seriously affected their investment. Back then what happened to the markets was a ‘shock’ as opposed to a ‘crash’ and, generally speaking, market shocks are short lived and can rebound very quickly which is exactly what occurred.

Any investor who decided to ‘come out’ of the market at that point would have missed the rapid improvement in the markets and would have lost the chance of recovering their losses. By being at the end of a phone those clients who were particularly worried about their investments were able to call us and be reassured that remaining invested was the best course of action and not be distracted by the news of, so-called, free-falling markets.

As Square Mile said in their recent stock market review ‘The stock market has beaten cash in 91% of all ten-year periods and although there are no guarantees as investments rise and fall, you are still likely to get back more than you put in – as long as you are patient’.

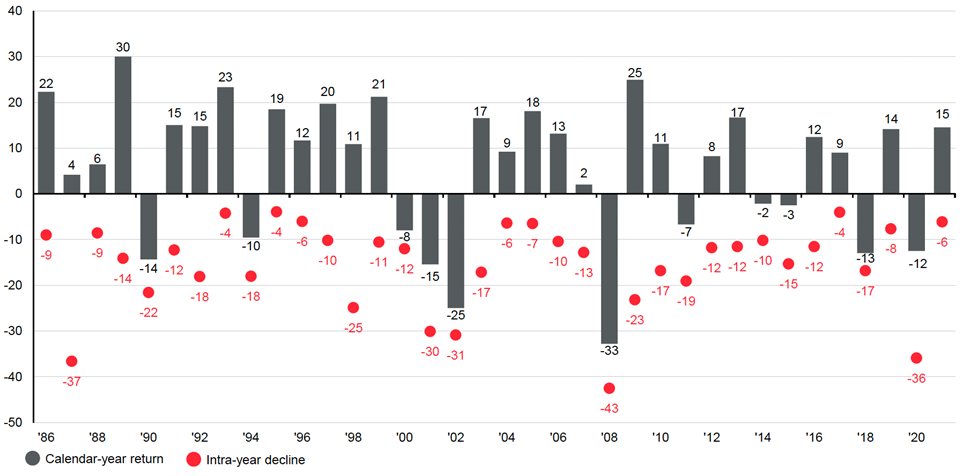

Finally, I thought I would finish with a graph, from the Square Mile stock market review demonstrating the importance of having patience and not making any knee-jerk decisions.

The below chart (reprinted with the permission of JP Morgan Asset Management) further demonstrates the despite average intra-year declines of 15.5%, annual returns of the FTSE All-Share have been positive over 25 out of 36 years.

FTSE All-Share intra-year declines vs. calendar-year returns

Source: FTSE, RefinitivDatastream, J.P Morgan Asset Management. Returns shown are price returns in GBP. Intra-year decline refers to the largest market fall from peak to trough within the calendar year. Returns shown are calendar years from 1986 to 2021. Past performance is not a reliable indicator of current and future results.

Call John Velasco, one of our independent financial advisers, for more information on investing your cash. Contact the office on 01329 282882 or send a message to our Facebook or Contact Us page.

Deposits provide capital security. Investments carry risk. The value of your investment (and any income from them) can go down as well as up and you may not get back the full amount you invested. Investments should be considered over the longer term and should fit in with your overall attitude to risk and financial circumstances.