Watching the Autumn budget in November, the Chancellor kept saying about putting more money into our pockets by lowering national insurance to help the economy grow…

The theory behind this is the more money we have in our pockets the more we spend.

This, in turn, increases the overall tax take to the government as when we buy things we tend to pay other taxes like VAT. It is a great theory, but very hard to make work as there is a lot that is out of the government’s control.

Policies like this rely on faith that we will spend more and history tells us that is not always the case.

So, there is an element that the government can control – the lowering of national insurance, and the element they can’t control – people spending more.

This got me thinking about pensions and investment products and how this theory can also apply in this area as well.

This is the case with the charges we pay for a product and the performance we get for the price we pay. This is so similar to what the chancellor has done today because one element is with our control and that is the charges you pay, and the other relies on faith in others to do what you expect/hope they will do to get great performance.

This got me thinking about why we do this and not just focus on the elements we can control.

When it comes to pensions and investments the only element we can control is charges, so lets look at that.

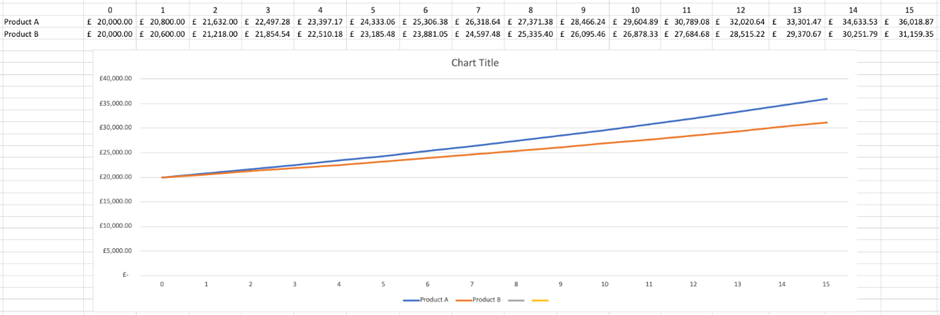

Let’s look at two products Product A and Product B both with £20,000 invested over 15 years:

Product A has ongoing charges of 1% per annum.

Product B has ongoing charges of 2% per annum.

If we assume that both products perform at a gross 5% per annum then, minus the charges, the outcome could be as follows:

This shows that over 15 years the same amount of money for 2 products that produced the same gross performance have vastly different values. Product B that is higher charging has a value that is over £5,000 less than Product B.

For Product B’s value to match Product A it would have to perform 1% better every year for 15 years. That is a lot of faith to put in someone and something that you have no control over, and that ultimately the person you put faith in has no control over.

This isn’t to say that paying more in the hope of better performance is the wrong thing to do or paying less to control what you can is the right thing to do because, as with everything in life, this is an individual decision personal only to you.

When you next look at this, or talk to an adviser, make sure you make a decision having all the facts and information. You can then make an informed decision knowing the potential outcomes and how they fit in with your goals.

You can contact our independent financial adviser, Dan Prosser, on 01329 282882 or via our Facebook or Contact Us page.

Past performance is not a guarantee of future results, and investing in the stock market always carries some degree of risk. The content of this article is for general information only and does not constitute advice.

The value of your investment (and any income from them) can go down as well as up and you may not get back the full amount you invested. Investments should be considered over the longer term and should fit in with your overall attitude to risk and financial circumstances.