What is The Workplace Pension?

You may have started to see the TV adverts with the big fluffy monster, called The Workplace Pension. He wanders around and is ignored by those he meets. You may have even wondered what it was all about!

A workplace pension is a system of saving for your retirement. Under the Pensions Act 2008 every employer must create a pension scheme that both the employee and employer contribute to.

How does The Workplace Pension affect me as an employer?

By 2018 all employers must automatically enrol you into a pension scheme – known as auto-enrolment.

Each company will receive a staging date, which is a date by which the scheme must be active. The individual dates are phased across the year so that it can be managed.

However, in the three or so years between October 2012 and January 2016, there were less than 40,000 employers reaching their staging date. In August 2017 alone there are 250,000 employers staging in that one month!

There is the option to postpone the assessment of your workforce by up to 3 months, but not the staging date and any employee can ask to be in the scheme during postponement.

How does The Workplace Pension affect me as an employee?

Not everyone will receive a workplace pension; the main exclusions are if you are not designated as a ‘worker’ under EU law (which means you could be employed or self-employed, as a contractor) or due to leave the company. For a full list of exclusions check out:

Joining A Work Place Pension – www.gov.uk

You will be automatically enrolled in the workplace pension providing you fit into the following criteria:

- You are classed as a worker

- You are aged between 22 and the state pension age (based on your gender and date of birth)

- You earn at least £10,000 per year

- You usually work in the UK

Other ‘workers’ designated as Non-Eligible (outside above criteria but within certain limits) will be given the option to auto enrol and have the employer contribute.

Other ‘workers’ designated as Non-Eligible (outside above criteria but within certain limits) will be given the option to auto enrol and have the employer contribute.

When the workplace pension scheme is due to start you will receive a letter from your employer outlining the details of the plan and when it is due to start. It will also confirm which category you fall into – Eligible job holder, Non-Eligible job holder or Entitled worker.

Tax relief is available with all employee contributions, whether you pay tax or not, as long as your employee has chosen the correct scheme for the staff he employs.

You have the option to opt out within a month of being auto-enrolled, but any inducement to do so is illegal and is punishable with fines.

It is important to note that you cannot opt out until you have been auto-enrolled in the scheme. Opting out is not recommended, as the long-term benefits outweigh the minimal disadvantages (i.e. small reduction in salary).

What does this actually mean?

Mary has been in her current job for 5 years as an accounts administrator for a small building firm. She earns £20,000 per year. Her boss has recently told her that she will be joining the new workplace pension scheme and as part of that, they will both contribute towards it.

Mary’s first question is how much is this going to cost her each month?

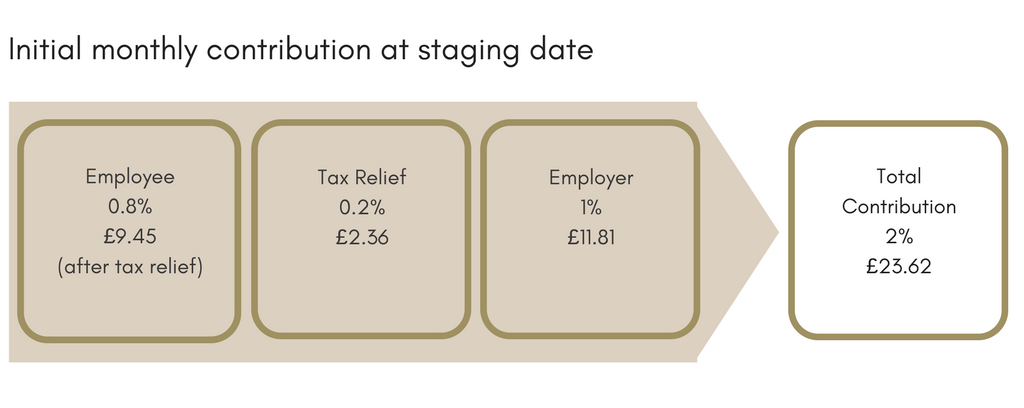

Currently, the schemes are being phased in. The initial contribution for most schemes is1% Employee contribution (0.8% after tax relief) with 1% Employer contribution.

This is based on Qualifying Earnings, the money earned between £5,824 pa (lower level) and £43,000 (top level). Mary’s qualifying earnings are £14,176pa. Broken down into monthly payments it looks like this:

So for a contribution of £9.45 each month, Mary will receive £23.62 into her pension scheme each month.

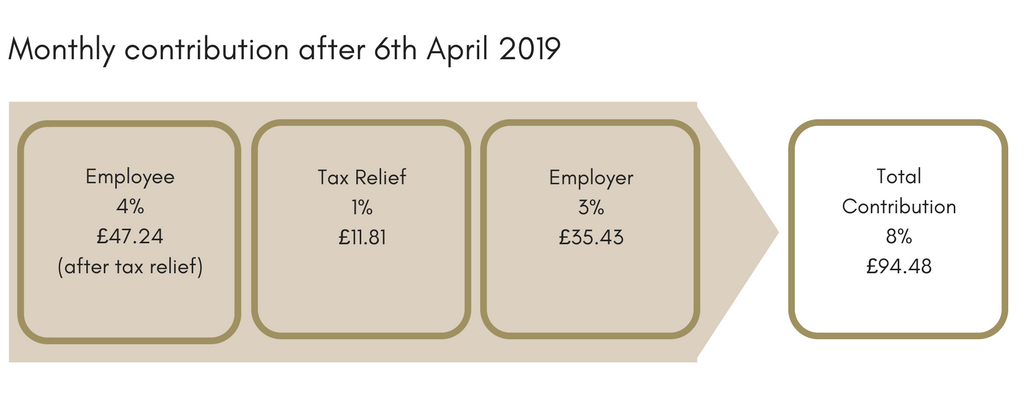

The amount contributed will increase (phased in) over time until it reaches its final % on the 6th April 2019, when all workplace pensions will be up and running.

A year of contributing 4% of her salary will mean that Mary receives over £1100 into her pension pot. When she receives a pay rise the contributions will also rise.

The role of the Independent Financial Adviser

Dealing with the complex pension systems, knowing your options and the process can be time-consuming. As Independent Financial Advisers (IFAs) we can guide employers through the process and advise on the best workplace pension scheme for your company, ensuring that the deadlines are met and the costs to the company are kept in check.

We can also run seminars with your employees on behalf of the company. We will talk them through the process and how it is offered as there are usually many questions associated with this change.

Our IFAs are available to discuss your personal situation outside of the workplace, to ensure that your whole retirement plan is best suited to you.

In Summary Neil, our Chartered Financial Planner comments…

I would advise all Employers not to ignore this because something that is very easy to put in place for a relatively small cost can be undone by ignorance.

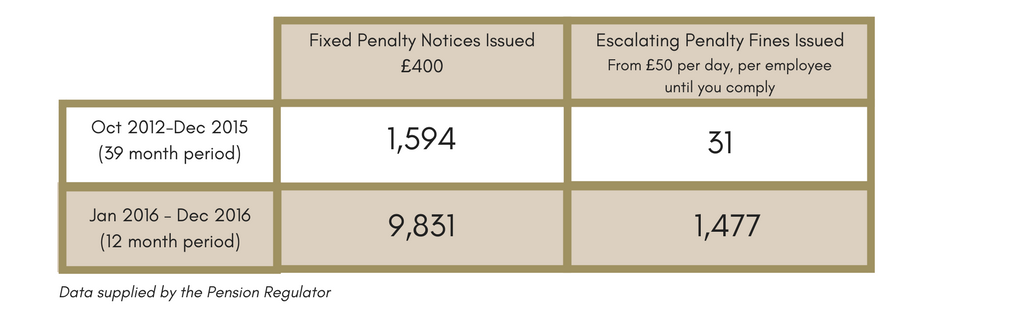

The fines for non-compliance are designed to hurt until you do comply:

Data supplied by the Pension Regulator

Data supplied by the Pension Regulator

The table shows a 516% increase in £400 fines in one year and over a colossal 46,000% increase in escalating fines in the same one year compared to the previous three. These are mainly small businesses on which these fines have a large impact.

Remember the staging date (go live date) cannot be changed. Postponement relates to your duty to assess your workers.

By law it is your responsibility to prove which workers should not be included in your scheme, should you be challenged. You must be able to prove that any self-employed staff under contract are not ‘workers’ under the EU definition.

By law it is your responsibility to prove which workers should not be included in your scheme, should you be challenged. You must be able to prove that any self-employed staff under contract are not ‘workers’ under the EU definition.

It is not enough to just say they are self-employed. If they are found to be ‘workers’, they will have to be auto-enrolled and the Employer will have to make good any back payments…as well as the appropriate fine!

You will be surprised at how easy it is to get advice, set up and comply, but don’t leave it to the last minute or try to ignore it…it won’t go away.

Pensions are a long-term investment. The fund can go up as well as down. Your final income at retirement age will depend on the fund size, interest rates and tax legislation at that time.

The Workplace Pension – Further Reading

Joining A Work Place Pension – www.gov.uk

Automatic Enrolment – www.pensionsadvisoryservice.org.uk

Contribution Pension Schemes – www.moneyadviceservice.org.uk

Jargon Buster

Auto-enrolment – a Government initiative to help people save for retirement through an automatic pension scheme at work.

Staging Date – the first date that an employer must comply with the legislative requirements for auto-enrolment.

Defined Contribution Scheme – a type of retirement plan in which both the employer and employee make regular contributions to.

Qualifying Earnings – the name given to a band of earnings you can use to calculate contributions for auto-enrolment. For the 2016/17 tax year, this is between £5,824 and £43,000 a year. The figures are reviewed annually by the government.

Eligible Job Holder – an employee who meets the criteria and will be automatically enrolled into the pension scheme

Non-Eligible Job Holder – an employee who is outside the criteria but has the option to voluntarily opt in and receive employer contributions

Entitled Worker – an employee who is outside the criteria but has the option to join without receiving an employer contribution

Pensions are a long-term investment. The fund can go up as well as down. Your final income at retirement age will depend on the fund size, interest rates and tax legislation at that time.

The Financial Conduct Authority does not regulate Workplace Pensions

The information is based on our current understanding of HM Revenue & Customs guidance as of 2016 / 2017.

Reference to tax reliefs are dependent on your own personal circumstances which are subject to change.